Key Takeaways

- Infrastructure debt provides contractual, senior-secured cash flows backed by essential service assets with historically lower default incidence than corporate credit (Moody’s Analytics, 2020).

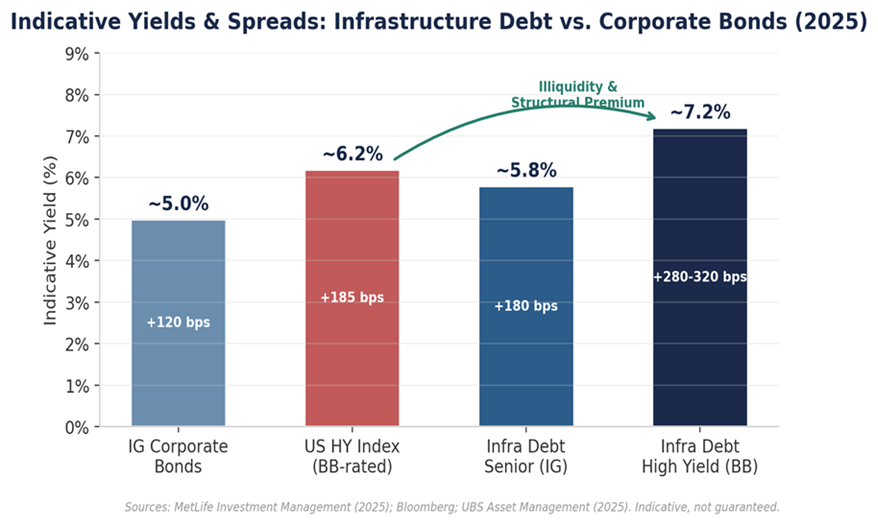

- Private market spreads typically exceed public high yield, reflecting illiquidity and structural complexity rather than incremental credit risk alone (MetLife Investment Management, 2025).

- Structural tailwinds — including bank retrenchment, refinancing needs, and energy transition investment — are expanding the opportunity set for private lenders (Macquarie Asset Management, 2024; UBS Asset Management, 2025).

- Risks remain sector- and manager-specific, particularly around construction, regulation, refinancing, and liquidity.

- For many institutional investors, infrastructure debt can function as a complementary income and diversification sleeve rather than a substitute for traditional bonds.

With real yields compressed in traditional fixed income and volatility elevated across public equities, investors are increasingly prioritizing assets that deliver predictable income with lower drawdown risk.

Infrastructure debt — lending to essential service assets such as utilities, transportation networks, renewable energy platforms, and digital infrastructure — has emerged as one such segment. Despite its scale and long operating history, allocations remain modest across institutional portfolios. Private infrastructure accounts for roughly 4% of allocations, with debt comprising only a portion of that exposure (Hodes Weill & Cornell University, 2024).

For allocators seeking contractual cash flows, inflation linkage, and structural seniority, infrastructure debt is increasingly viewed as a complementary sleeve alongside traditional credit and private markets strategies.

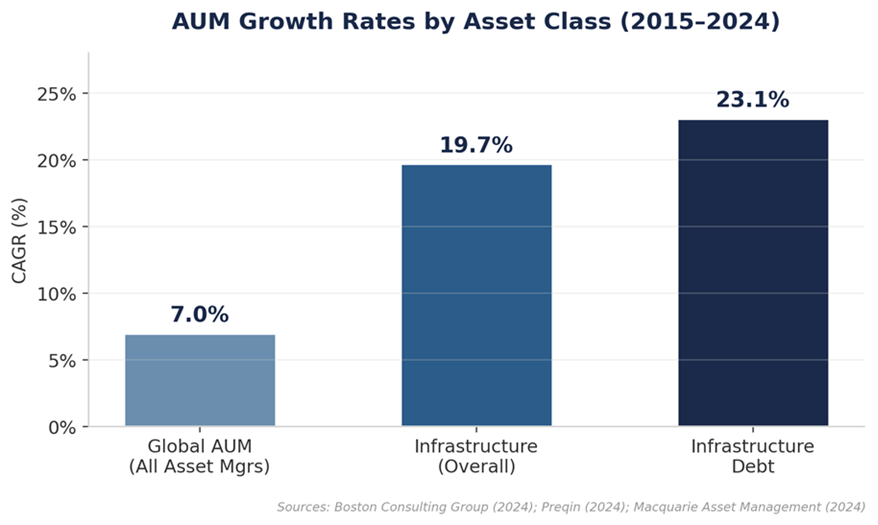

Figure 1: Infrastructure debt has grown at nearly 3x the pace of global asset management AUM since 2015.

Structural Foundations

Infrastructure assets differ meaningfully from conventional corporate borrowers. They typically provide essential services with low demand elasticity, operate under regulated or contracted revenue regimes, and require significant upfront capital with high barriers to entry (Macquarie Asset Management, 2024). Together, these features support durable, visible cash flows across cycles.

For lenders, this translates into structural protections that are less common in corporate credit markets: senior secured positions, long-term concession or offtake agreements, dedicated liquidity reserves, and, in many cases, explicit inflation pass-through mechanisms.

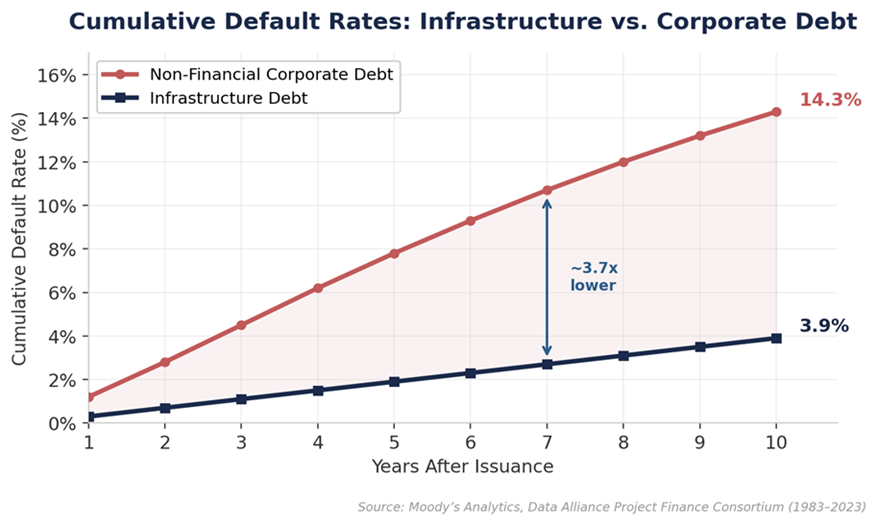

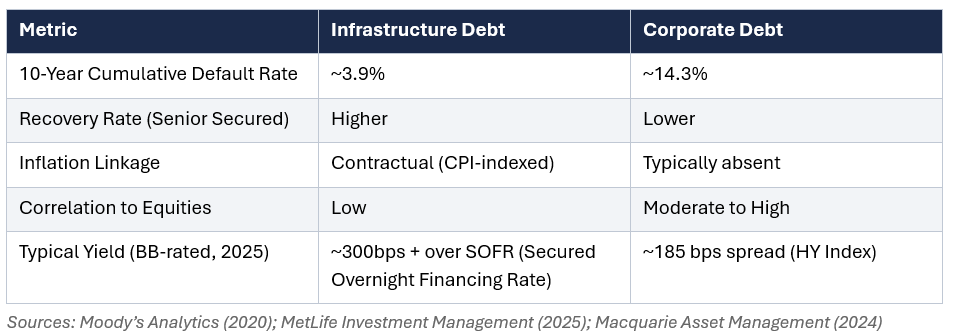

Historically, this structure has been translated into lower credit losses. Moody’s data indicates cumulative default rates for infrastructure project debt of approximately 3.9% by year 10, compared with roughly 14.3% for non-financial corporate credit (Moody’s Analytics, 2020).

Figure 2: Infrastructure debt exhibits significantly lower cumulative default rates than non-financial corporate debt.

Relative Value in Today’s Market

Private infrastructure debt typically prices at wider spreads than similarly rated public credit, reflecting illiquidity, structural complexity, and reduced bank competition for long-duration assets.

Recent market pricing has placed BB-rated private infrastructure spreads in the high-200s to low-300s basis points over SOFR, implying all-in yields of approximately 7% or higher. For many investors, this represents incremental carry relative to public high yield, supported by stronger collateral and covenant protections.

Comparisons, however, are most meaningful on a net basis. Fees, liquidity constraints, and manager selection materially influence realized returns, and private market volatility is often smoothed relative to public benchmarks. As such, infrastructure debt is best evaluated as a differentiated private credit exposure rather than a direct substitute for liquid bonds.

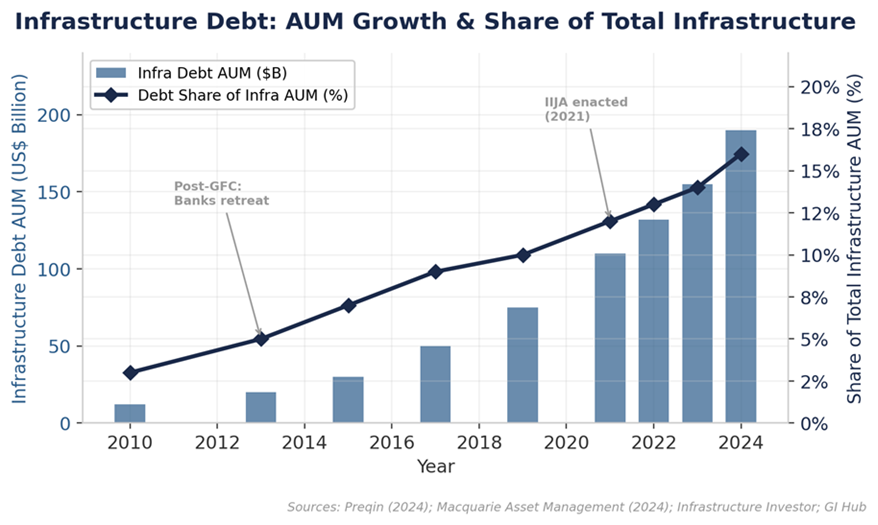

Figure 3: Infrastructure debt AUM has grown substantially since the post-GFC bank retreat, now representing ~16% of total infrastructure assets.

Figure 4: Infrastructure debt offers meaningful yield premiums over comparable corporate credit, reflecting illiquidity and structural premia.

A Growing Opportunity Set

Several structural forces continue to expand the opportunity set for private lenders.

Global infrastructure requirements continue to rise, driven by energy transition, grid modernization, digitalization, and transportation upgrades. At the same time, regulatory capital constraints have reduced banks’ appetite for long-dated project finance, creating space for institutional capital providers to step in at attractive terms. A wave of refinancing across maturing assets is further contributing to consistent deal flow.

The result is a deeper and more diversified pipeline spanning renewable power, energy storage, data centers, fiber networks, utilities, and social infrastructure.

Risk and Underwriting Considerations

Although default incidence has historically been lower than in corporate credit, risks remain material and vary meaningfully by sector and structure.

Construction execution, regulatory or tariff resets, demand variability, refinancing conditions, and limited secondary liquidity can all affect outcomes. Performance dispersion across managers is also significant, reflecting differences in sourcing, structuring, and asset oversight.

For these reasons, realized returns depend heavily on disciplined underwriting and portfolio construction. Infrastructure debt should be viewed as private credit with real asset characteristics — offering enhanced income potential in exchange for reduced liquidity and greater complexity.

Portfolio Applications

Focused on senior secured, contracted, or brownfield assets, infrastructure debt can serve multiple roles within diversified portfolios:

It can provide contractual income, introduce partial inflation sensitivity, diversify exposure away from listed markets, and offer downside protection through collateral and structural safeguards.

These attributes have supported growing allocations among insurers, pensions, endowments, and family offices seeking stable yield without assuming full equity risk.

Key Takeaway

Consolidated Investment Thesis – Infrastructure Debt

Infrastructure debt has evolved into a core segment of the private credit universe, offering a combination of long-dated contractual cash flows, senior secured positioning, and embedded inflation sensitivity that is increasingly scarce in public fixed income markets. Historical loss experience, essential-service revenue models, and conservative capital structures have underpinned resilient performance across cycles, while bank balance-sheet retrenchment and rising global infrastructure capital requirements continue to reinforce favourable supply–demand dynamics.

Positioned between traditional fixed income and private real assets, infrastructure debt blends predictable cash flows and structural protections with the inherent trade-offs of private markets—most notably reduced liquidity, greater underwriting complexity, and heightened manager-selection risk. Returns are therefore driven less by broad market beta and more by disciplined structuring, asset selection, and operator and counterparty assessment.

As institutional capital increasingly reallocates from public bonds toward private credit and real assets, infrastructure debt is transitioning from a niche allocation to a strategic portfolio building block. For investors able to underwrite its illiquidity and complexity, the asset class offers a differentiated source of durable income, inflation linkage, and portfolio diversification that is difficult to replicate in public markets.

Overweight senior secured, core and core-plus infrastructure debt within private credit allocations on a multi-year horizon. Favour contracted or regulated brownfield assets with CPI linkage and strong sponsor alignment. Prioritize managers with demonstrated sourcing, structuring, and restructuring capability. Maintain Neutral on construction-heavy or merchant-exposed strategies and Underweight highly levered or subordinated capital structures where return premia primarily reflect risk rather than illiquidity.

References

Hodes Weill & Cornell University (2024). Institutional Infrastructure Allocations Monitor. Program in Infrastructure Policy, Cornell University.

IFM Investors / Infrastructure Investor (2025). Infrastructure Debt Positioned Well for the Year Ahead.

Macquarie Asset Management (2024). Infrastructure Debt: First Among Equals. Macquarie Insights.

MetLife Investment Management (2025). Infrastructure Debt: A Compelling Private Credit Portfolio Addition. Markets Group Strategic Insights.

Moody’s Analytics (2020). Examining Infrastructure as an Asset Class. Moody’s Analytics Data Alliance Project Finance Consortium.

UBS Asset Management (2025). Infrastructure 2025 Outlook. Asset Class Perspectives.