Introducing multi-asset private market content in a modern portfolio have shown to add significant diversification benefits and may hence improve returns.

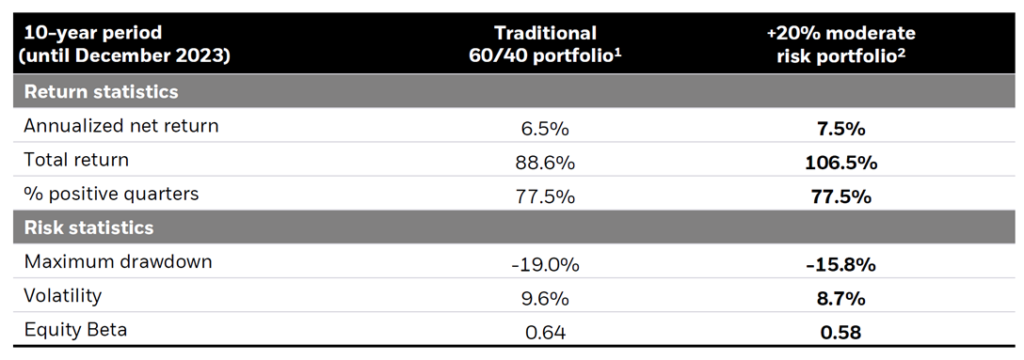

Illustrative Traditional 60/40 Portfolio Back Test – With a 20% Allocation to Moderate Risk Portfolio

Source: BlackRock and Partners Group – Solving the Private Markets Allocation Gap: From Products to Portfolio Construction, Sep 2024

As such, private markets and alternative investments have become central to modern portfolio construction. Yet despite their growing popularity, they remain among the most misunderstood components of family offices portfolios.

For many investors, private equity, private credit, real assets, and hedge funds are viewed primarily as return enhancers — vehicles to generate higher returns than traditional public markets. Institutional and sophisticated family offices, however, think differently.

For them, alternatives are not only about excess return: they provide structural portfolio resilience. Understanding this distinction is essential for family offices seeking institutional-grade outcomes, and surviving black swans.

Why Institutions Allocate to Private Markets

Leading endowments and sovereign investors allocate heavily to private markets for three core reasons:

- Access to differentiated return drivers

- Control over capital structure and cash flows

- Long-term alignment with illiquid opportunity sets

Returns matter — but they are not the starting point.

Institutional portfolios are built from first principles:

- How different assets behave across cycles

- How they interact under stress, and

- How they support long-term compounding

With relative flexibility in liquidity constraints and time horizons, private markets, when used correctly, can help address issues that public markets cannot.

The Illiquidity Premium: Real, Conditional, and Often Mispriced

The idea of an “illiquidity premium” is widely accepted, but rarely examined critically. Unpriced, unrewarded illiquidity are risks to be avoided and should not be awarded with any premium.

Illiquidity alone does not generate excess return. Investors are compensated only when they:

- Provide stable, patient capital over cycles, recognising geopolitical changes

- Absorb complexity or structural inefficiency

- Exercise governance or control

In practice, many family offices overpay for illiquidity by:

- Accepting long lockups without commensurate return, ie uncompensated risks

- Underestimating cash flow uncertainty

- Failing to size private allocations relative to true liquidity needs

These increases potential for liquidity constraints and unnecessary drawdowns. As such, institutions and sophisticated family offices need to evaluate illiquidity as a risk to be budgeted, not a feature to be embraced indiscriminately.

Private Equity: More Dispersion Than Premium

Private equity (PE) remains one of the most powerful — and polarising — asset classes.

Top performing managers continue to deliver strong outcomes, but the dispersion between top and bottom performers can be extreme. Median private equity returns often fail to even compensate adequately for leverage, fees, and illiquidity.

Institutional allocators should therefore focus on:

- Manager selection and access to deals

- Strategy fit within the broader portfolio

- Vintage diversification

- Capital pacing discipline

The most resilient PE portfolios are those that drive value through direct intervention. It is no longer enough to simply buy and hold.

PE is not a monolithic asset class – It is a collection of highly differentiated strategies, each with distinct risk characteristics, driven by operational growth, and not financial engineering.

Private Credit: The Rise of Contractual Income

As banks retreat from certain forms of lending, private credit has stepped up and grown rapidly. As such, institutions favour private credit not merely for yield. Other considerations include:

- Seniority in the capital structure

- Contractual cash flows

- Collateral protection

- Negotiated covenants

However, not all private credit is defensive. Risk varies significantly across:

- Senior vs subordinated lending

- Sponsor-backed vs asset-backed deals

- Cyclical vs non-cyclical borrowers

Used correctly, private credit can form the backbone of an income-oriented portfolio. Used poorly, it becomes risk in disguise.

Real Assets: Inflation Protection Requires Precision

Real assets — infrastructure, real estate, natural resources — are often marketed as inflation hedges. In reality, inflation protection is highly asset-specific.

Institutional investors distinguish between:

- Regulated vs unregulated cash flows

- Contracted vs market-priced revenue

- Operating vs development risk

Only assets with pricing power or contractual escalation offer reliable inflation linkage. Optical inflation hedges without cash flow certainty can fail precisely when they are most needed.

Hedge Funds and Liquid Alternatives: Risk Management Tools, Not Return Engines

In institutional portfolios, hedge funds are rarely expected to outperform equities over full cycles. Instead, they are used to:

- Reduce drawdowns

- Provide diversification during stress

- Manage volatility and tail risk

Return expectations are realistic. The value comes from how hedge funds behave when other assets struggle.

This framing is often missing in family-office allocations.

The Liquidity Illusion in Private Markets

One of the most common mistakes is confusing reported stability with actual economic stability.

Private assets only appear to be less volatile largely due to:

- Appraisal or contractual based pricing

- Infrequent valuation, with no daily mark to market values

- Lagged adjustments

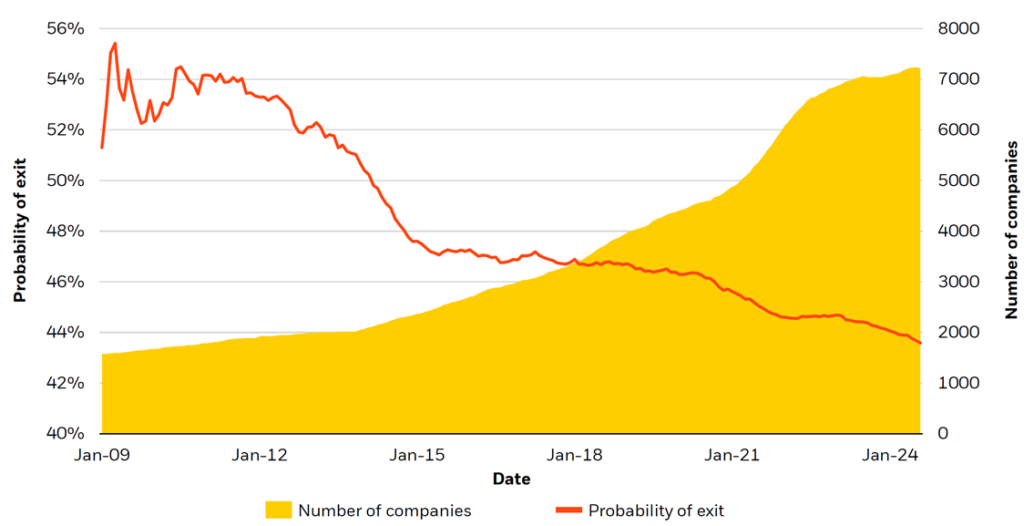

In reality, data over time has shown the number of private market exits decreasing. While the volume of companies in the venture and growth universe has increased, the worrying trend is that the quality of deals has decreased, ie less exit and hence, less liquidity.

Number of Exits Decreasing

Source: BlackRock – Private Markets Outlook 2026, A New Continuum

Institutions therefore manage private markets by:

- Stress-testing economic exposure

- Maintaining explicit liquidity buffers

- Limiting reliance on secondary liquidity assumptions

Liquidity management is not an operational detail — it is a strategic necessity.

How Institutions Integrate Alternatives into Portfolios

Rather than treating alternatives as a standalone bucket, institutions should:

- Allocate by risk contribution

- Integrate alternatives into total portfolio construction

- Evaluate interactions under stress scenarios

- Rebalance across cycles, not sentiment

Key Takeaway

Private markets can be powerful allies in long-term wealth creation — but only when approached with institutional discipline.

Family offices and institutions need to have:

- Clear objectives

- Realistic expectations

- Robust governance

- Patience paired with selectivity

The family offices that thrive over generations are not those with the most alternatives, rather those with the best-integrated portfolios.

In private markets, as in all investing, structure resilience undoubtedly matters more than stories and trends.

#PrivateMarkets #Alternatives #FamilyOffice #PrivateEquity #PrivateCredit #InstitutionalInvesting #PortfolioConstruction #FTCPInsights