For decades, real assets were sometimes treated as an optional niche allocation — useful for diversification, but could be replaced with bonds, rather than essentially central to portfolio construction. That has changed.

Today, leading endowments, sovereign funds, and sophisticated family offices are systematically increasing exposure to real assets, not as a tactical trade, but as a structural pillar of long-horizon portfolios.

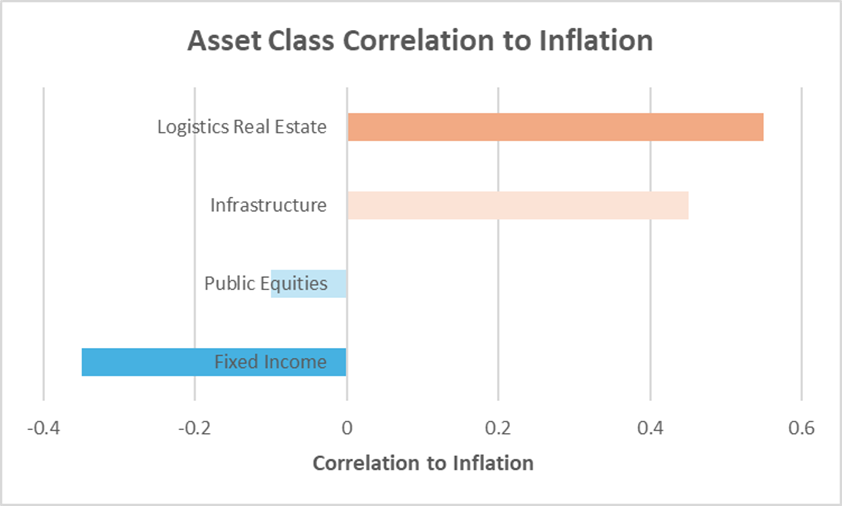

Why The Shift Is Happening Now

Three forces are driving this reallocation:

1. Inflation is no longer transitory

While headline inflation has moderated, significant structural inflation drivers — energy transition, supply chain restructuring, geopolitical pressures, demographics, and fiscal expansion — remain unchanged and firmly in place.

Real assets provide contractual or intrinsic inflation linkage that equities and bonds often fail to address.

Source: PGIM Quantitative Solutions 2024

2. Public markets are more correlated than assumed

During stress periods, the equity-bond correlation may turn positive, rendering diversification unreliable. Real assets — particularly infrastructure, real estate with pricing power, and natural resources — do not just have positive correlation to inflation, they are also distinct cash-flow drivers, reducing portfolio-level drawdowns.

3. Yield scarcity in traditional assets

With compressed real bond yields and elevated equity valuations, institutions are seeking durable, asset-backed income that does not rely on financial engineering.

What Real Assets Actually Mean Today

Institutional investors should take long-term and thematic views and not chase opportunistic real estate or cyclical commodities for short-term returns or yields. Instead, allocations need to consider geopolitical realities, technological advances and bifurcation, long-term structural changes and regionalisation of supply chain to focus on:

- Core and core-plus infrastructure, especially in regulated utilities, data centres, transportation, and renewables.

- Logistics and essential real estate with long leases and inflation-linked escalators.

- Energy transition assets with contracted cash flows with long-term viability.

- Selective natural resources tied to structural demand, especially critical minerals for the energy transition and advanced industries such as copper, lithium and rare earths.

The emphasis is on predictability, downside protection, and resilience over the long-term, not headline returns.

Portfolio Implications for Family Offices

For family offices, real assets should not be viewed just as a return enhancer, but as a risk-management tool:

- Stabilising portfolio income

- Reducing reliance on public market beta

- Improving real returns over cycles

As such, manager selection, leverage discipline, asset quality, and governance determine whether real assets protect wealth, or amplify risk.

Key Takeaway

Institutions increasing real asset exposure are not making a tactical call — they are adapting to a new investment regime. Family offices that continue to rely solely on financial assets may fall behind structurally, risking increased volatility and lower returns.

Real assets are no longer optional. They are essential fundaments.

#PrivateEquity #PrivateCredit #Alternatives #FamilyOffice #AssetManagement #Realasset #FTCPInsights