For decades, conservative portfolios were built on a simple assumption: buy high-quality bonds, hold blue-chip equities, and rely on mean reversion. That playbook worked – until valuations across almost every major asset class climbed to historic extremes and previous assumptions are now being challenged.

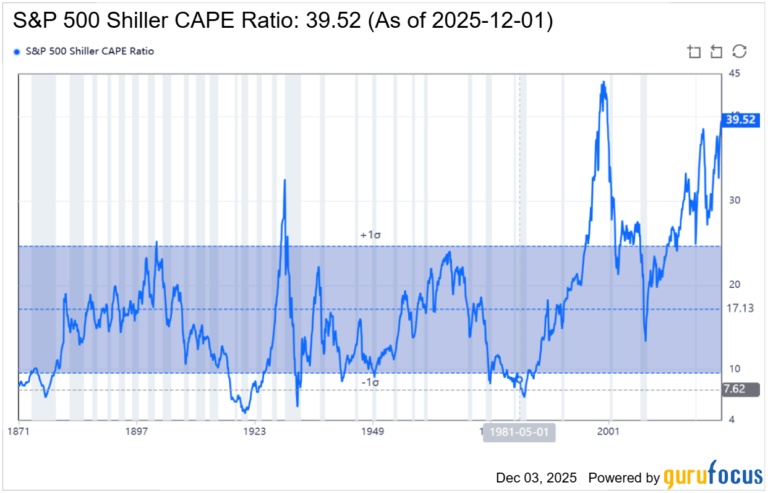

The current Cyclically Adjusted Price-to-Earnings (CAPE) ratio for the S&P 500 is 39.52, more than doubled that of the historical median of 16.04. This suggests that the market is quite overvalued.

There has been chilling comparisons of the current market to the tech bubble in 2001 in view of the similar patterns that have emerged. As such, designing a conservative portfolio today for capital preservation and for defensive purposes needs a new playbook: precision, discipline, and institutional-grade portfolio engineering.

- High Valuations Demand Lower Forward Returns

When valuations stretch, investors can expect future returns to become asymmetric: limited upside, and meaningful downside. Family offices with long horizons must thus adjust expectations:

- Equities priced at 20 – 30x earnings cannot realistically deliver 8–10% long-term returns.

- Bonds are no longer a free hedge, and duration can cut both ways.

- Traditional 60/40 has become valuation-dependent and needs to be revisited carefully for each investor.

A conservative portfolio should now behave like an endowment, not a traditional passive policy portfolio.

- Risk Management Is Not Market Timing

It may not be sensible to depend on strategies that include “waiting for a crash”. Timing the market do not consistently yield positive outcomes. It is about risk-aware portfolio design:

- Reduce uncompensated risk exposure.

- Increase diversification across uncorrelated alternatives.

- Use systematic risk controls to avoid fat-tail events.

Institutions outperform not because they take less risk, rather it is because they take designed and calculated risks, not random risks.

- Alternative Income from Structural, Not Cyclical Sources

Conservative portfolios still require yield. However, reaching for credit beta or duration may not be prudent. Instead, one can explore yields from:

- Senior secured private credit

- High-quality infrastructure debt

- Real-estate backed income streams, such as REITS

These offer yield without equity-like drawdowns.

- What are the Objectives?

The objectives for a conservative portfolio should minimally include:

- Capital preservation

- 3 – 5% income

- Maintenance of liquidity

- Avoidance of drawdowns that impair multi-generational wealth

The new conservative portfolio should to be institutional, diversified, and data-driven.

Key Takeaway

Old rules were built for a world of low valuations and high yields. Today’s environment demands a new playbook – one that treats risk management as a science, return as an outcome, and resilience as the core mandate.

#PortfolioStrategy #AssetAllocation #GlobalMarkets #FamilyOffice #AssetManagement #FTCPInsights