Quantitative investing has evolved from a niche strategy into a component of many institutional portfolios.

Today, many of the world’s largest asset managers and hedge funds rely on quantitative models to analyse markets, manage risk, and construct portfolios.

Yet many may not understand what the advantages and limitations of quantitative investing.

What Quantitative Investing Really Means

At its core, quantitative investing is a data-driven, rule-based approach that uses mathematical and systematic modeling, computer algorithms, and massive datasets to identify, analyze, and guide investment decisions.

These models can be used to:

- Identify factors that drive long-term returns

- Detect pricing anomalies in markets

- Construct diversified portfolios

- Manage risk exposures

The goal is not to eliminate human judgment, but to systematise parts of the investment process.

The Benefits of Systematic Approaches

Quantitative strategies offer several advantages:

- Reduced bias: Models follow predefined rules, reducing behavioural biases.

- Scalability: Quantitative systems can analyse thousands of securities simultaneously, with strategies able to be applied across numerous asset classes and geographies.

- Speed of analysis: Automated systems can process vast amounts of data and execute trades rapidly quickly.

- Risk Management: Advanced techniques are used to analyze market risk and manage overall portfolio risks and diversification.

These characteristics make quantitative strategies particularly effective in highly liquid markets.

The Limits of Quantitative Models

Despite their strengths, quantitative models do have major limitations that investors should be cognisant of. Without understanding their constraints and incorporating appropriate risk control parameters can result in major drawdowns when model fails in unforeseen circumstances.

- Model Risk: Models are based on historical data that may not predict future performance, especially during unprecedented market events.

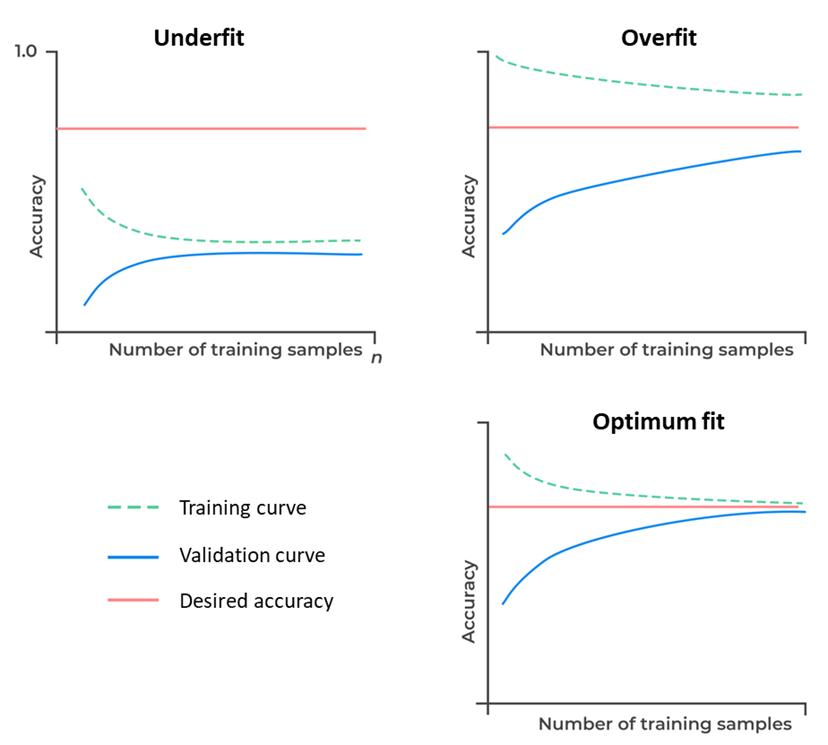

- Overfitting: When a model is over-trained to be too tailored to past data, it performs exceptionally well in back-testing, but fails in real-time and predictive outcomes.

Learning Curves: Accuracy in Validation and Training Samples vs Training

Source: Overfitting and Methods of Addressing It, Analyst-Prep CFA level 2, 6 Mar 2021

- Data Dependency: A strategy is only as good as the input data. Inaccurate, incomplete, or delayed data can lead to poor investment decisions.

- Lack of Flexibility: Models may fail to adapt to sudden, qualitative market shifts such as geopolitical events that were not incorporated present in the training data.

- Lack of Causal Understanding: Quantitative models identify correlations, not causation. This can lead to failure to understand impact of structural changes in a company’s business model that a qualitative analyst might pick up.

As a result, investors need to combine quantitative tools with discretionary oversight.

The Hybrid Future

The future of investing is unlikely to be purely quantitative or purely discretionary.

Instead, the most effective organisations need to integrate both approaches — using models to process information efficiently while relying on human judgement to interpret broader economic dynamics.

Key takeaway

Quantitative investing is not about replacing investors with algorithms. It is about augmenting human decision-making with systematic insight.

#Fintech #AI #InvestmentTechnology #FamilyOffice #AssetManagement #QuantFinance #FTCPInsights