Some investors believe in gaining an edge through accurate forecasting, ie predicting recessions, anticipating market tops, forecasting inflation, and timing re-entry points. It is intuitively appealing and tempting – promising protection in downturns and amplifying returns in recoveries.

The challenge lies not in theory, but in what happens in real life and the immense difficulty in execution.

Yet when we examine the practices of the world’s most successful long-horizon investors — endowments, sovereign wealth funds, and leading family offices — a different reality emerges.

Their advantage rarely comes from prediction.

It comes from systematic risk control.

Among the most powerful — and underutilised — of these tools is volatility targeting. Volatility-based frameworks have helped institutional portfolios survive crises, compound capital, and avoid the behavioural traps that derail many investors.

For single family offices thinking in decades rather than quarters, understanding this distinction is critical.

The Persistent Illusion of Market Timing

To succeed at timing, an investor must be right twice:

- When to exit to reduce risk

- When to re-enter

Even sophisticated investors struggle to do this consistently. Empirical evidence shows that:

- Some of the strongest market returns occur immediately after periods of extreme stress

- Missing a handful of recovery days can permanently impair long-term returns

- Emotional decision-making often overrides rational analysis at precisely the wrong moment

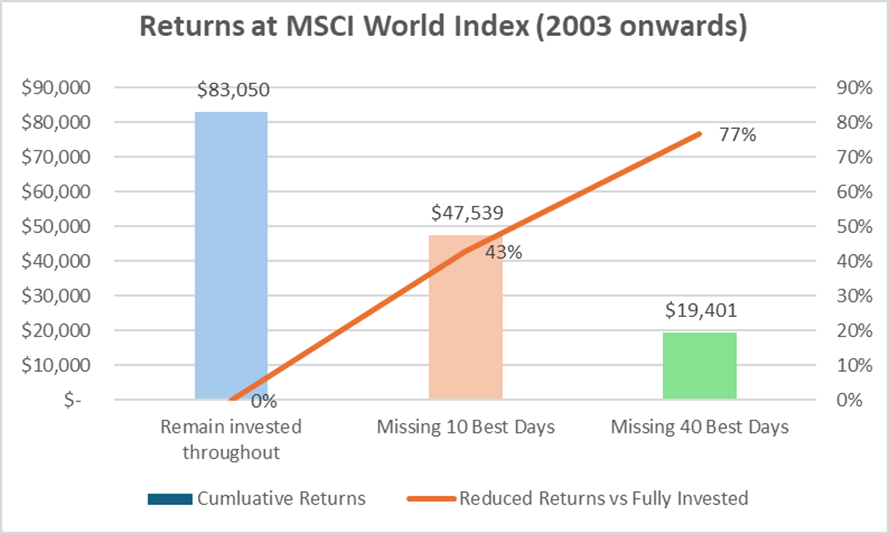

Data has shown that missing just 10 best days out of more than 22 years, or only 0.18% of all trading days, invested in the market, will yield 43% less return, compared to simply remain invested throughout the highs and lows during the whole time.

Missing out 40 best days or 0.4% of all trading days will yield 77% less return.

Source: Datastream – Daily returns of the MSCI World index unhedged from 31 Oct 2003 to 2 Jan 2026

As such, in practice, market timing often converts temporary volatility into permanent loss.

This is not a critique of intelligence or experience. It is a recognition of structural and behavioural limits.

Why Long-Term Capital Suffers from Timing Errors

Family offices face unique challenges that make market timing particularly dangerous:

- Concentrated wealth amplifies emotional pressure, increasing behaviour gaps

- Multi-generational objectives increase the cost of drawdowns

- Governance structures while crucial can inadvertently slow decision-making during fast markets

- Capital preservation mandates limit tolerance for recovery risk

In these environments, a single poorly timed decision can undo years of disciplined compounding.

This is precisely why institutions must evolve away from prediction-based strategies.

What Is Volatility Targeting

At its core, volatility targeting is a risk-first framework.

Instead of allocating capital based on expected returns or market views, portfolios are constructed around a target level of risk. This should be based on each family office’s risk appetite and risk budget, bearing in mind volatility and drawdown tolerance.

The central question shifts from: “Where do we think markets are going?”

to: “How much risk should we take given current market conditions?”

When volatility rises:

- Exposure is reduced incrementally

When volatility falls:

- Exposure is increased prudently

It should be emphasized that the aim of volatility target is not to supercharge returns, and it may even lower performance in the short-term. The main objective is to prevent losses from becoming unrecoverable by:

- Reducing maximum drawdowns

- Reducing likelihood of extreme negative returns

These thus will lead to improvement in the overall return-to-maximum drawdown, ie better risk-adjusted returns and especially important for family offices that prioritize capital preservation.

Why Volatility Is a Superior Risk Signal

Volatility is not a forecast – It is a real-time signal of market stress, leverage, and uncertainty.

Historically, periods of elevated volatility coincide with:

- Tightening liquidity

- Rising correlations across asset classes

- Forced deleveraging

- Behavioural panic

By responding to volatility rather than predicting outcomes, portfolios adapt dynamically to changing risk regimes.

This adaptive quality is what gives volatility targeting its structural advantage.

The Institutional Case for Volatility Targeting

Endowments and sovereign investors favour volatility-based frameworks for several reasons:

1. Drawdown Control

Large drawdowns require exponentially higher returns to recover. Reducing drawdown severity thus improves long-term compounding more reliably than chasing upside.

2. Behavioural Discipline

Rules-based exposure adjustments reduce emotional decision-making during crises, preventing behaviour gaps.

3. Faster Recovery

Portfolios with controlled drawdowns regain previous peaks faster, even if headline returns appear lower in bull markets.

4. Governance Compatibility

Volatility frameworks align naturally with investment committees, risk budgets, and policy portfolios; it compliments and supports risks management policies.

In short, volatility targeting can help to structure how long-term capital is governed.

Volatility Targeting in Practice for Family Offices

Volatility targeting does not require high-frequency trading nor complex derivatives. It can be implemented at multiple levels:

- Portfolio-Level Volatility Caps: Set an explicit volatility range for the total portfolio and adjust exposures when breached.

- Risk Budgeting Across Asset Classes: Allocate risk, not capital, across equities, credit, alternatives, and real assets.

- Dynamic Exposure Bands: Allow asset weights to flex within predefined ranges based on volatility conditions.

- Diversification by Risk Driver: Combine strategies with different volatility and correlation profiles to stabilise overall risk.

The key is clarity and consistency, not complexity.

The Role of Alternatives in Volatility-Managed Portfolios

Private markets and alternatives play an important role — but they must be understood correctly. While private assets often report lower volatility, this is frequently due to:

- Appraisal smoothing

- Infrequent pricing (not mark to market, but contractual)

- Structural illiquidity

Institutions therefore assess economic volatility, not reported volatility, when integrating private assets into volatility-targeted frameworks.

For family offices, this means:

- Stress-testing private exposures

- Avoiding over-reliance on “optical stability”

- Ensuring liquidity buffers are sized appropriately

Volatility targeting is about assessing true risk, not reported comfort.

Common Misconceptions About Volatility Targeting

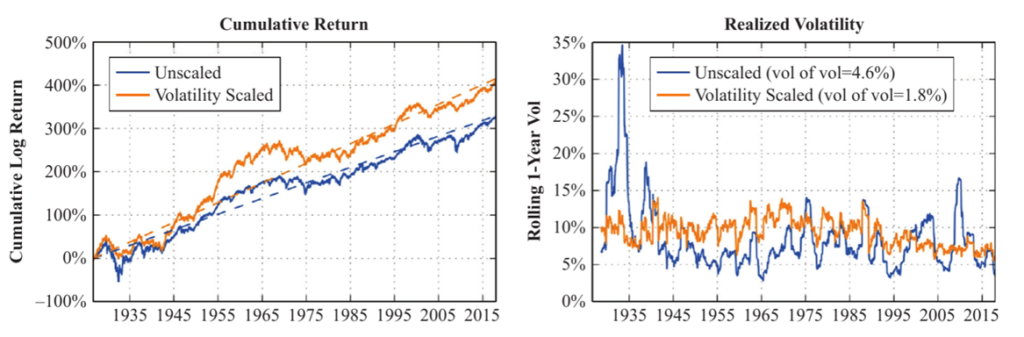

- “It sacrifices upside”

In strong bull markets, volatility-managed portfolios may lag slightly. Over full cycles, however, improved drawdown control often leads to superior compounded returns.

Cumulative Returns and Realised Volatility for US Equities (1927 – 2017)

Source: The Journal of Portfolio Management – The Impact of Volatility Targeting, Fall 2018

As observed from the cumulative returns for US Equities above, volatility scaled portfolios yielded higher returns compared to unscaled ones over the long-term.

- “It is too conservative”

Volatility targeting does not mean low risk — it means appropriate risk, suitable for investors with stewardship for multi-generation wealth preservation and growth.

- “It requires constant intervention”

Well-designed frameworks operate with periodic rebalancing, not daily trading.

Why This Matters More in the Coming Decade

The next decade is likely to feature:

- Higher macro volatility

- Geopolitical uncertainties

- Less reliable diversification, ie correlations between different asset classes may turn positive

- More frequent regime shifts

In such environments, prediction becomes harder — not easier.

Risk management therefore transform from being a defensive exercise to possibly an important source of alpha.

A Structural Advantage for Multi-Generational Wealth

For families with a 30-, 50-, or 100-year horizon, the goal is not to simply maximise returns in any single year. It is to:

- Avoid catastrophic loss

- Maintain decision discipline

- Preserve optionality

- Enable steady, long-term compounding

With such objectives, volatility targeting can be an important tool for sophisticated family offices and institutions.

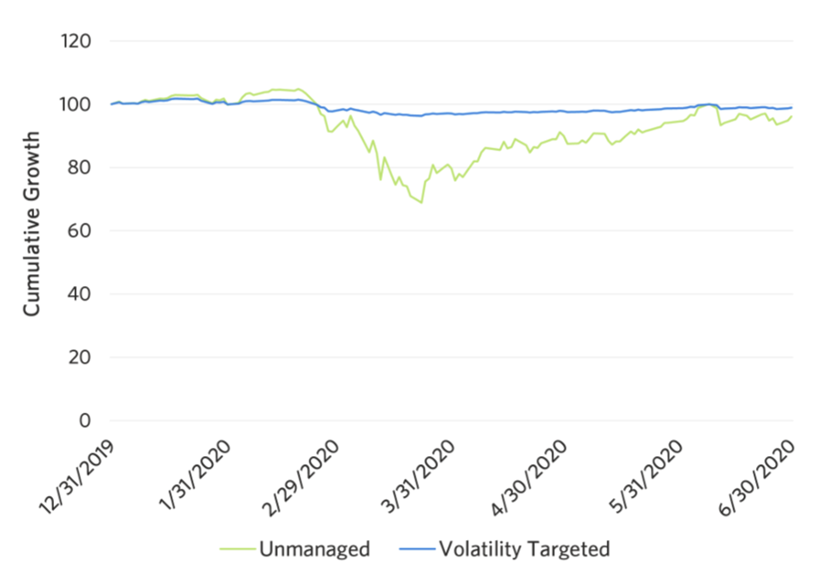

Taking the COVID crash as a case study, a volatility-unmanaged portfolio saw losses of close to 25% while the volatility targeted portfolio was down less than 5%. Although by the end of June, both strategies were virtually at the same level, investors that panicked would have sold, or been forced to sell, during such a drawdown.

Portfolios of family offices and institutions that have adopted volatility targeting would have been positioned to avoid such permanent losses.

COVID Crash Comparison

Source: Research Affiliates – Harnessing Volatility Targeting in Multi-Asset Portfolio, Jan 2024

Key Takeaway

Market timing is seductive, intuitive — and unreliable.

Volatility targeting is methodical, unemotional, and structurally aligned with long-term capital stewardship. The most successful family offices of the next generation will not be those that predict markets best, but those that manage risk most consistently.

In a world of uncertainty, risk control is not a constraint on returns — it is the foundation of capital preservation and growth.

#Inflation #IncomeInvesting #Volatility #FamilyOffice #AssetManagement #RiskManagement #VolatilityTargeting #LongTermInvesting #FTCPInsights