Many Family Offices believe their portfolios underperform because they did not pick the right stocks or missed the latest investment trend. The truth is simpler — and far more important: they are taking risks that do not pay them.

Institutions call this uncompensated risk — risk that increases volatility, but does not increase expected return. This is what silently undermines returns one expects from long-term compounding.

1. Concentration Risks Disguised as Conviction

Family portfolios often resemble a collection of “favourite ideas” accumulated over time. This results in:

- Over-exposure to specific themes

- Idiosyncratic risk from individual positions

- “Home bias” toward domestic equities or real estate

This is not conviction. It is portfolio fragility.

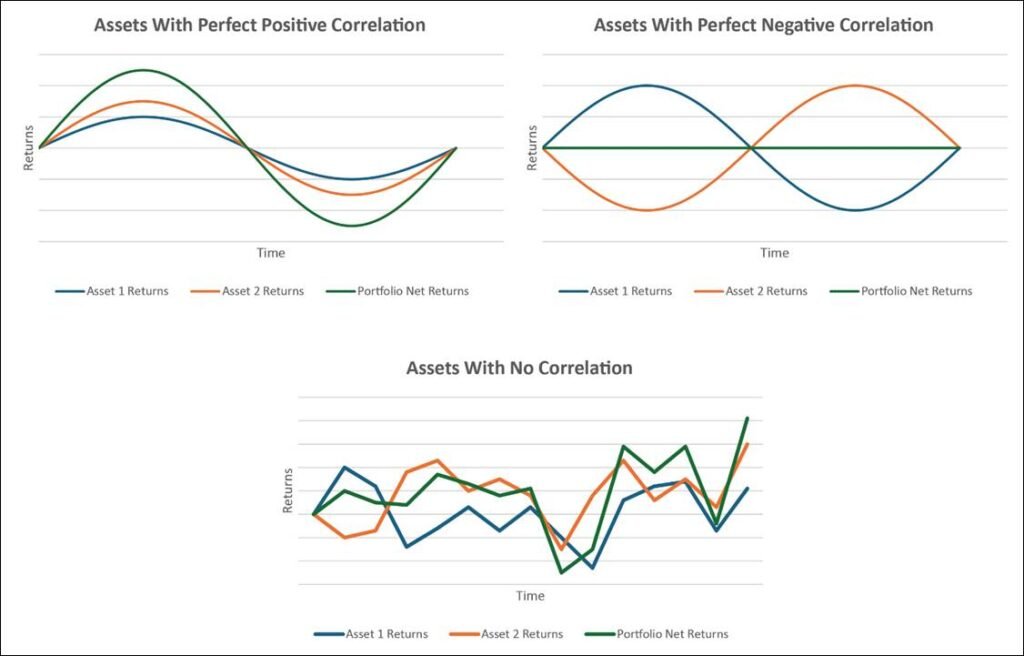

2. Importance of Correlation

The correlation between different assets in the overall portfolio is crucial to overall portfolio net returns. A portfolio with highly correlated assets can have its net returns enhanced in good times, but likewise it can also produce heightened losses when the tide turns.

As such, when designing the constitution of any portfolio, investors should be mindful of the impact of correlation. Many Family Offices, however, may lean heavily on asset classes that they are more familiar with; when stress hits, exposures can positively correlate sharply and exacerbate losses.

To mitigate this, diversify with investments that have low correlation, which may include alternatives such as private credit, infrastructure, real asset and hedge-style diversifiers.

3. Excess Cash Is Also a Form of Risk

Holding large cash balances feels safe, but across the long term, cash:

- Drags down on real returns

- Lowers long-term purchasing power due to inflation

- Becomes a barrier to proper rebalancing and compounding

Institutions rarely hold more than 2 – 3% cash unless strategically needed.

4. Lack of Formal Risk Budgeting

Endowments and sovereign funds begin with a simple question: “How much risk can we afford to take, and where should that risk be allocated?”

Families rarely operate with such frameworks.

Without proper risk budgeting:

- Portfolios develop unintended exposures

- Drawdowns become unpredictable

- Returns become inconsistent and luck-dependent

5. The Solution: Paid Risk, Not Random Risk

Institutional-grade portfolios focus on risks with positive long-term premia:

- Equity beta (at reasonable valuations)

- Credit spreads

- Illiquidity premium

- Real-asset income

- Duration at the right point in the cycle

- Adjust portfolio to account for the correlation of individual investments on a portfolio basis

It is essential to remove the noise. Keep the premia.

Key Takeaway

Most portfolios underperform not because Family Offices lack access to opportunities, but because they carry unpriced, unrewarded risks.

Fix this, and performance improves — not by taking more risk, but by taking the right kind.

#RiskManagement #InvestmentInsights #InstitutionalInvesting #FamilyOffice #AssetManagement #FTCPInsights