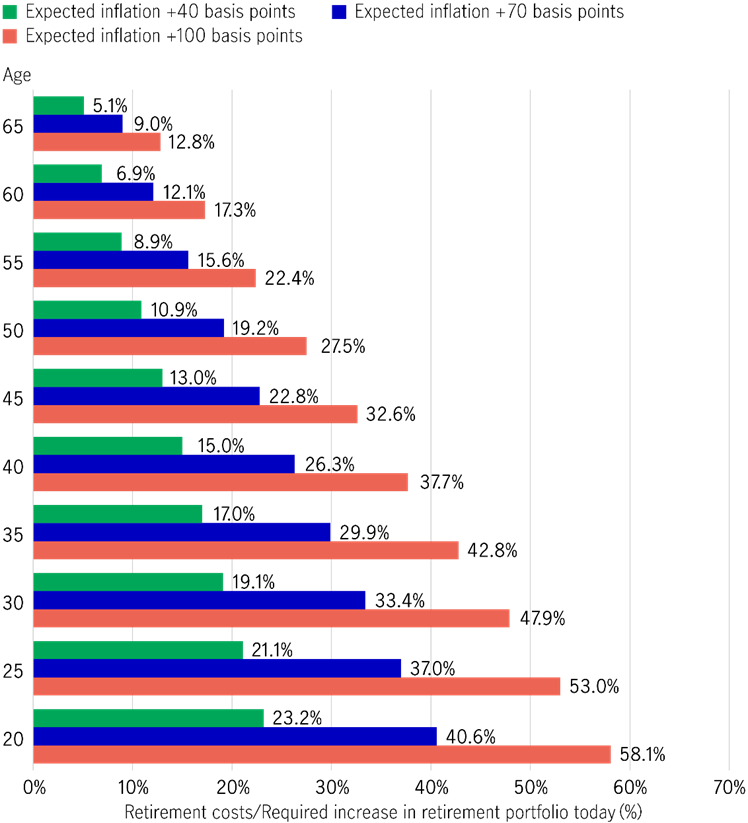

Inflation has a material and significant impact on investment returns and retirement costs. Even a small modest expected inflation has a substantial impact to retirement costs.

Effect of Rising Inflation on Retirement Costs

Source: Manulife Investments – Plan for Retirement with Inflation in Mind, 23 Jan 2024

Therefore, inflation and how best to contain it has always been a key mandate for central banks.

For many developed countries in the recent decades, inflation has been in check, and many may even have assumed that inflation is merely cyclical and can be easily contained – until recently.

While short-term pressures may ease, the long-term forces driving inflation appear to be structural and persistent.

Portfolios built for the low inflation era must thus adapt.

Why Inflation Is Structurally Higher

Key drivers include:

- Deglobalisation and supply-chain redundancy

- Energy transition and infrastructure spending

- Heightened capital expenditure in AI technologies

- Labour shortages in ageing economies

- Persistent fiscal deficits

These forces raise the floor of inflation, even as volatility remains.

Why Traditional Hedges Fall Short

Many portfolios still rely on:

- Long-duration bonds

- Equity growth exposure

- Static real estate allocations

In inflationary environments, these can fail simultaneously — especially when valuation multiples compress.

How Institutions Are Adapting

Sophisticated investors are shifting from nominal hedges to real cash-flow protection, including:

- Infrastructure with regulated or contractual inflation pass-through, such as utilities, data centres and transportation

- Real estate with pricing power and short lease durations, including logistics and supply chain plays

- Private credit with floating-rate structures

- Select commodities tied to long-term thematic demand, like critical minerals and rare earths

The focus is not on speculation, but cash-flow durability.

Portfolio Construction Implications

Inflation-aware portfolios:

- Reduce reliance on duration

- Increase exposure to real assets and floating-rate income

- Stress-test real returns under multiple inflation scenarios

This approach acknowledges uncertainties and how inflation can erode nominal returns, rather than forecast them away.

Key Takeaway

Inflation is no longer a tail risk. It is a core design factor that should be embedded in all portfolios.

#Inflation #IncomeInvesting #Volatility #FamilyOffice #AssetManagement #FTCPInsights