Many family offices articulate a clear objective: achieve 4 – 5% real returns or more over the long term, while preserving capital. Far fewer portfolios consistently deliver it.

The gap is not due to lack of sophistication — but to structural design flaws.

Why Most Portfolios Miss Real-Return Targets

The common mistakes are predictable:

- Over-reliance on equity beta

- Excess exposure to nominal bonds

- Underestimation of inflation drag

- Underrate how volatility impacts return

- Poor diversification within alternatives

In practice, portfolios are often built for optimistic environments, not resilient outcomes.

How Institutions Engineer Real Returns

Endowments that meet real-return targets do not chase simply performance. They engineer portfolios around three core principles:

1. Multiple independent return engines

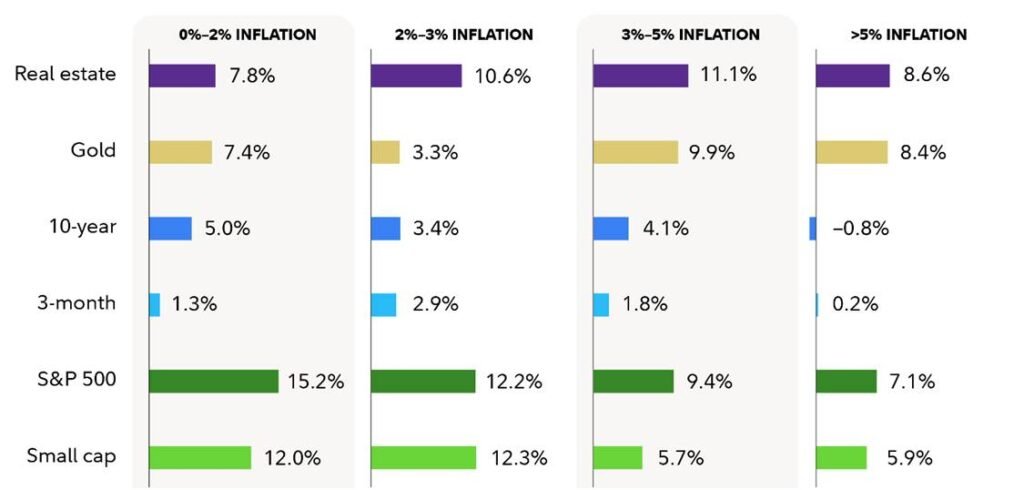

Should a portfolio be concentrated in any one asset class, returns over a short timeframe may yield desirable returns. However, over time – especially in high inflationary environments – the real returns are bound to fall below expectations.

How Select Asset Classes Have Performed in Different Inflation Ranges (1960 – 2024)

Source: Fidelity – 7 Ways to Inflation-Proof Your Portfolio, 7 May 2025

Instead, returns need to be sourced from a wider pool, including alternatives:

- Private credit and contractual yield

- Private equity in high-conviction themes

- Real assets with inflation linkage

In the current rapidly changing macro environment, uncertainties abound and significant impact on returns are not just possible, but should be structurally accounted for. As such, no single engine should dominate – diversification is key.

2. Inflation-aware construction

Nominal returns are irrelevant if purchasing power erodes. Institutions explicitly model:

- Inflation sensitivity by asset class

- Real cash-flow durability

- Pricing power at the asset level

3. Risk budgeting, not asset allocation

Capital is allocated based on risk contribution, not labels. This prevents hidden concentration in correlated assets masquerading as diversification.

What Actually Works in Practice

Successful real-return portfolios typically share these characteristics:

- Equity exposure capped and diversified globally

- Meaningful allocation to private credit, private equity and real assets

- Limited use of leverage

- Rebalancing driven by risk, not market narratives

Importantly, volatility is controlled not through timing, but through structural diversification.

Implications For Family Offices

For family offices, the question is not whether 4 – 5% real returns are achievable — they are.

The real question is how the portfolio can be intentionally designed, instead of assembled incrementally, to ultimately achieve such an outcome.

Key Takeaway

Real returns are not a product of forecasts or market timing. They are the outcome of discipline, design and structural robustness.

#Inflation #IncomeInvesting #Volatility #FamilyOffice #AssetManagement #FTCPInsights