Introduction

As we enter into 2026, global investors face one of the most challenging macro environments of the past decade. Inflation has moderated, but may remain uneven across regions, bearing in mind lag effects from the tariffs. Interest rates are moderating, but decline may not be uniform. Geopolitical risks continue to reshape supply chains, capital flows and investment frameworks. Yet beneath the uncertainties lie a clear opportunity: long-duration patient capital that positions early will be best placed to capture the structural shifts now underway.

For single family offices, UHNW investors and institutional allocators in Asia, 2026 is set to be a year where portfolio resilience, selective risk-taking, and strategic reallocation matter more than tactical timing.

This article distils the most important trends that will shape investment decisions in 2026 — and how sophisticated investors should respond.

1. A Slower but Stickier Rate-Cut Cycle

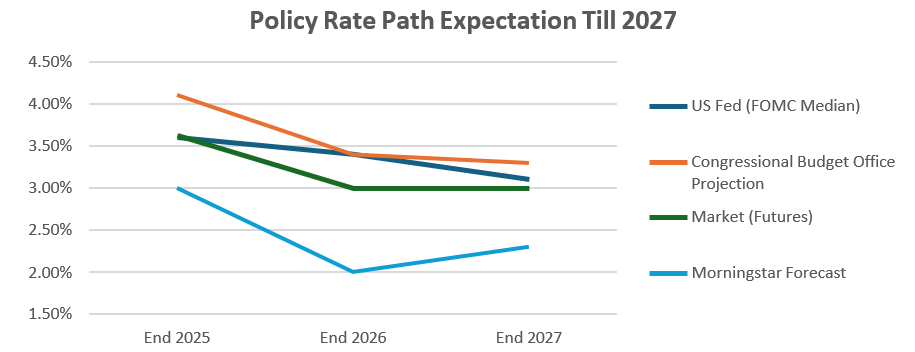

Investors have been waiting for global rate cuts since early 2024. While the US and Europe are expected to cut rates in 2026, the path may be slower and shallower than previously expected.

Sources: 1. Federal Reserve and Congressional Budget Office announcements (Aug – Dec 2025). 2. Forbes – What to Expect for Interest Rates in 2026, 29 Nov 2025. 3. Moringstar – How Much will Fed Cut Interest Rates, 26 Jun 2025

Key forces driving this shift:

• Labour markets remain tight

• Energy prices remain volatile

• Fiscal spending continues to run high

• Productivity gains from AI are real, but scenarios to achieving returns are still unclear

What this means for investors

• Bonds to be back in focus, with attention on spreads and duration gaining attention.

• Private credit remains attractive, and segments of the market remain under accessed.

• Equity valuations for value and quality vs growth.

2. Private Equity: Asia Poised for a Rebound

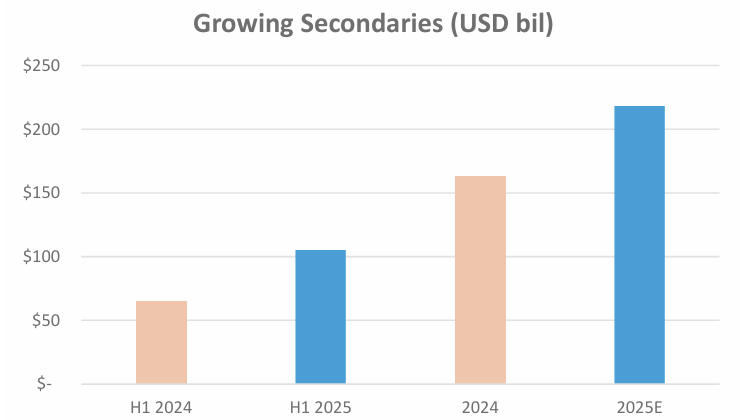

Private equity in Asia saw a sharp slowdown through 2022–2023, but deal activity recovered in 2024 and accelerated in 2025. This growth is expected to strengthen into 2026.

With an increasing need for the return of capital to LPs, liquidity is gaining attention, shifting focus to secondaries and continuation funds. Progressive rebound in exits in the coming years is expected, which will allow private equity fundraising to restart.

Source: 1. Jefferies H1 2025 Secondary Market Review, July 2025. 2. Jefferies – Global Secondary Market Review, July 2024 (based on closed deal volume). 3.Greenhill 1H 2025 Global Secondaries Market Review. 4. Preqin, as of July 2025. Buyout, venture, growth, and secondaries.

Drivers of the rebound:

• Lower financing costs

• Strong regional markets in Southeast Asia, India and Japan

• Regionalisation of supply chains

• Growing LP appetite for non-USA deal flow

Sectors expected to outperform:

• Advanced manufacturing

• Healthcare & med-tech

• Digital infrastructure

• Renewable energy transition

Investor takeaway

For family offices, small-mid buyouts and structured minority deals offer attractive risk-adjusted returns. Allocators should favour managers with sector depth and local sourcing capabilities.

Secondaries can offer flexible portfolio management for private wealth participation and regional diversification in 2026.

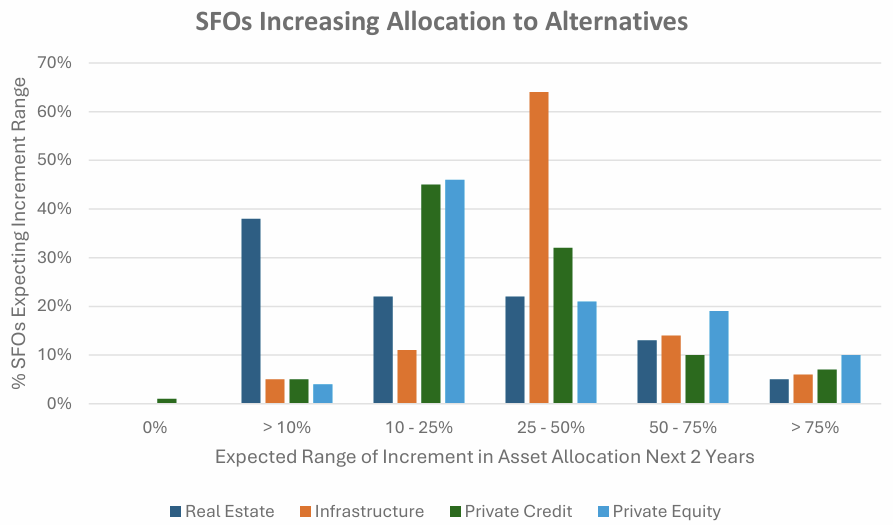

3. Family Offices Increasing Allocations to Alternatives

Global family office surveys have shown an increasing allocation to alternatives, driven by the search for stable yield and uncorrelated returns.

Key shifts observed:

• Alternatives rising from 32% in 2015 to >45% in 2024

• Private credit and infrastructure gaining the fastest share

• Declining allocation to traditional 60/40 portfolios

• Greater interest to leverage patient capital for thematic longer duration strategies

Source: Ocorian – Diversification Boosts Family Office Exposure to Alternative Assets, 12 Aug 2025

Investor takeaway

2026 will be the year where portfolios become more barbelled:

• Short-term liquidity needs: Core income (credit, infrastructure, dividend equities)

• Long-term asset growth: Targeted high-alpha strategies (venture, growth equity, secondaries)

4. China: Capital Flows Will Resume, But Differently

2026 will mark a turning point for China-related investments — not a return to the past, but the emergence of a new framework for allocating capital.

Themes to watch:

-

China’s ODI approval regime stabilising

-

Higher scrutiny of round-trip investment structures

-

Domestic restructuring creating opportunity

-

Foreign investor presence becoming more strategic than opportunistic

Investor takeaway

The smartest capital is shifting from macro-beta China exposure to micro-alpha opportunities: restructuring, carve-outs, distressed partnerships, and deep-technology supply chain investments.

5. Structural Trends That Will Define Long-Term Returns

Looking beyond short-term macro noise, several themes will shape returns over the next decade:

A. AI Productivity & Digital Transformation

Adoption will accelerate across healthcare, logistics, industrials and education.

B. Demographics & Aging Economies in Asia

Healthcare, age-tech, and senior-living assets will attract institutional capital.

C. Supply Chain Regionalisation

Southeast Asia becomes a long-term manufacturing and investment hub.

D. Energy Transition & Infrastructure

Sustained multi-trillion-dollar capital formation across Asia.

Conclusion: 2026 Favors Prepared, Patient, Long-Term Investors

The best opportunities in 2026 will not come from chasing momentum, but from positioning early in secular trends while balancing liquidity, yield and risks.

For family offices and institutional-grade investors, the most important actions now are:

- Re-optimise strategic asset allocation

- Increase exposure to alternatives prudently

- Build optionality across Asia’s growth corridors

- Focus on managers and investments with true operating depth

The year 2026 will reward sophistication, not speculation.

#TailRisk #PortfolioResilience #WealthManagement #FamilyOffice #AssetManagement #FTCPInsights