Rethinking the Illiquidity Premium

The era of easy money — where returns were driven by cheap leverage and rising market multiples — came to an end.

With higher entry multiples, exit delays and lower investor distributions, investors are re-evaluating the illiquidity premium for private equity (PE).

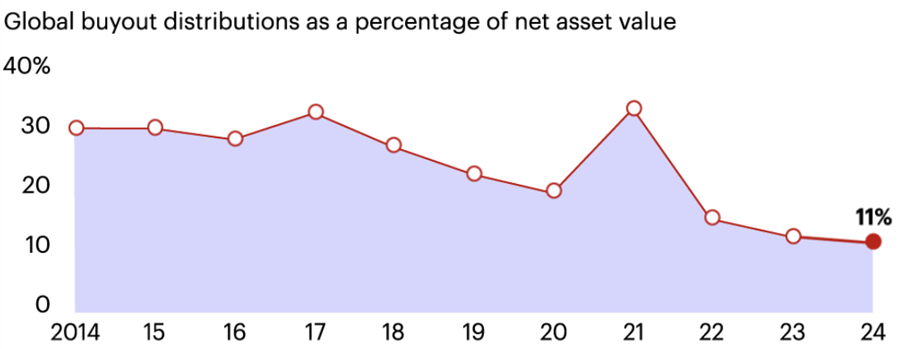

Distributions to Investors Hit a Low

Source: Bain – Global Private Equity Report 2025.

Why PE Matters

Despite tighter exit environments, PE continues to offer advantages that public markets may not match:

- Active Ownership

- Long-Term Horizon (no quarterly earnings pressure)

- Access to Innovation

Recent PE Developments

Investors need to be cognisant of recent market developments and possible elevated risks:

- Rising entry valuations

- Exit routes, timelines and returns are less predictable

- Highly levered deals with refinancing and default risks

- Vintage concentration without pacing discipline

This does not mean PE is broken — it means selectivity matters more than ever.

How PE Can Work

The most resilient PE portfolios are those that drive value through direct intervention. It is no longer enough to simply buy and hold:

- Operational Transformation: Improving governance, digitalizing supply chains, and professionalizing management teams.

- Sector-Specific Conviction: Focusing on high-conviction themes – with geopolitics an important consideration – such as USA reshoring, supply-chain relocation, and the China tech bifurcation.

- Strategic Exit: Understanding the nuances of regional exchanges and growing appetite for cross-border M&A in fragmented markets.

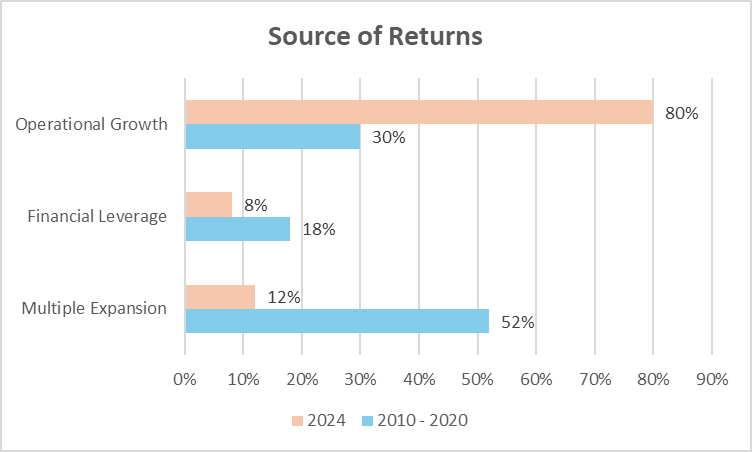

Source: Bain & Company Global PE Report 2024.

The illiquidity premium is very much alive, but it must be created by the manager. For family offices, this means moving beyond allocating to passive managers toward a more active, strategic approach to PE that prioritizes tangible value-add over simple capital injection.

Portfolio Construction Matters

PE serves as a major driver for capital appreciation. It provides a higher return potential in exchange for lower liquidity, making it ideal for the growth core of a multi-generational portfolio.

However, the biggest mistake family offices can make is over-allocating without:

- Liquidity planning

- Vintage diversification

- Realistic cashflow forecasting

As funds are locked up for a substantial timeframe and exits could be delayed, liquidity considerations are essential – buffers should be in place for cashflow contingencies.

What Distinguishes Institutional-Grade PE

PE still belongs in institutional portfolios — but only when:

- Expected returns justify illiquidity

- Manager skill is demonstrable – operational strength and proprietary sourcing of off-market deals

- Portfolio liquidity remains resilient under stress

- Exit discipline

Key Takeaway

Success in PE now depends on operational growth, not multiple expansion or financial engineering. The primary focus should be on managers who can demonstrate a repeatable process for operational excellence to improve margins and scale revenues.

#PrivateEquity #PrivateCredit #Alternatives #FamilyOffice #AssetManagement #FTCPInsights